In the auditing profession, technical competence is merely the entry requirement. The true hallmark of a high-quality auditand the primary defense against material misstatement is the effective exercise of professional judgement. Recognizing that poor judgement is a recurring theme in quality failures, the Financial Reporting Council (FRC) issued comprehensive guidance in June 2022 to provide auditors with a structured, rigorous approach to decision-making.

While this guidance is non authoritative, it encapsulates “good practice” that the FRC expects firms to analyze and integrate into their own internal frameworks. We have summarised some of their key points, however please refer to the document in the link above to read their full guidance.

Understanding the Framework

The FRC defines professional judgement as the application of relevant training, knowledge, and experience within the context of auditing, accounting, and ethical standards to make informed decisions. This isn’t just about “big” decisions like going concern; it permeates every level of an audit, including resourcing, task allocation, and firm-level quality management.

The FRC’s framework is built upon four pillars designed to ensure consistency and quality:

1) The Auditor’s Mindset

A robust judgement begins with the right mental posture. The framework identifies five critical mindset aspects:

Public Interest Benefits: Understanding that the audit acts for the benefit of intended users helps motivate objectivity and a commitment to quality.

Professional Scepticism: Maintaining a questioning mind and critically assessing evidence is vital, especially when challenging management assertions.

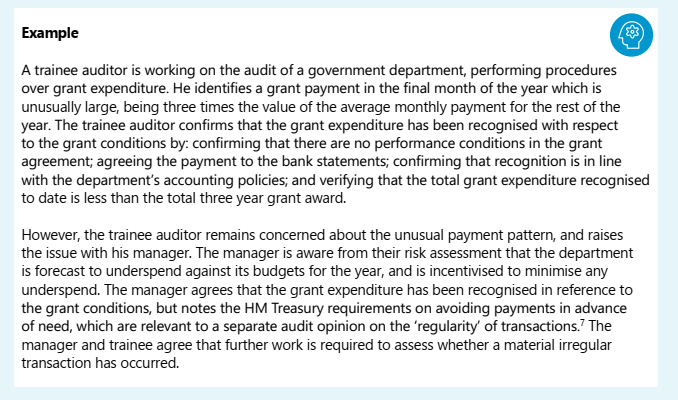

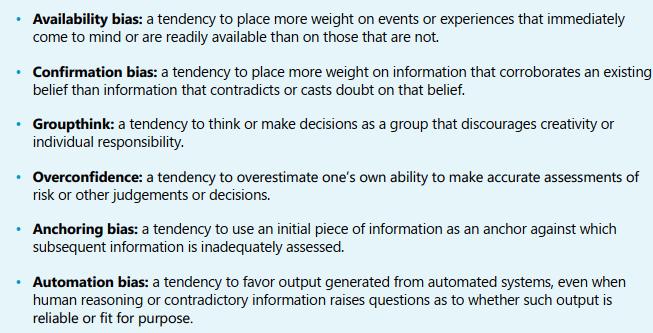

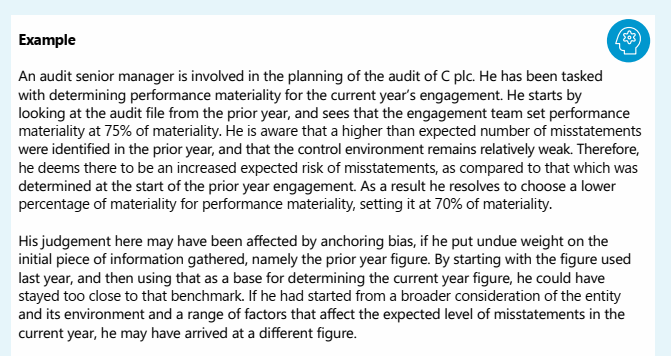

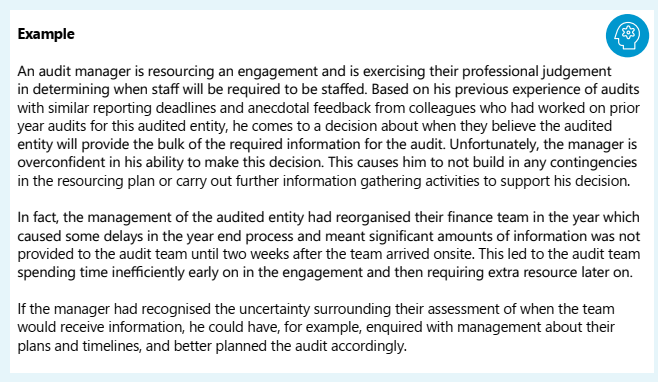

Psychological Factors and Bias Awareness: Auditors must actively guard against “judgement traps” and bias:

Sensitivity to Uncertainty: Acknowledging that information sources vary in reliability and that some outcomes are inherently uncertain allows for better risk management.

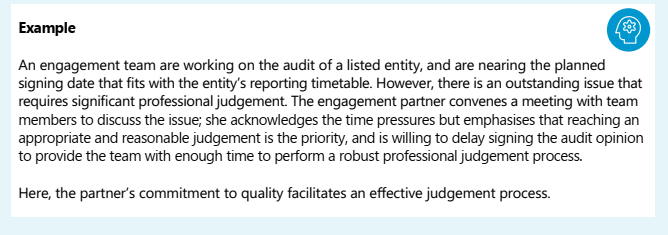

Commitment to Quality: Prioritizing a robust process over time or budget pressures is essential for reaching reasonable conclusions.

The Professional Judgement Process

While judgement is rarely linear, the FRC suggests a structured process for complex issues:

Trigger: Remaining alert to situations that require more than an intuitive evaluation.

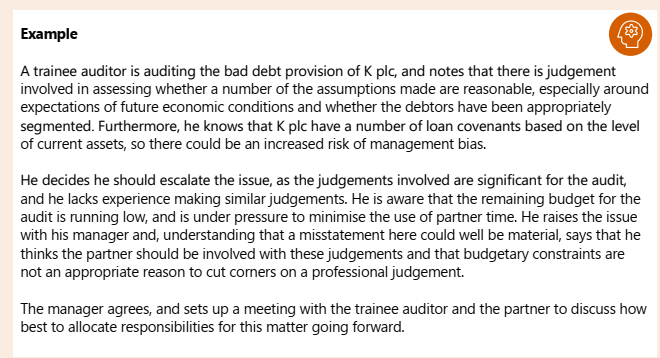

The Right Person: Ensuring the individual making the decision has the necessary skills and resources, and escalating issues when they exceed one’s experience.

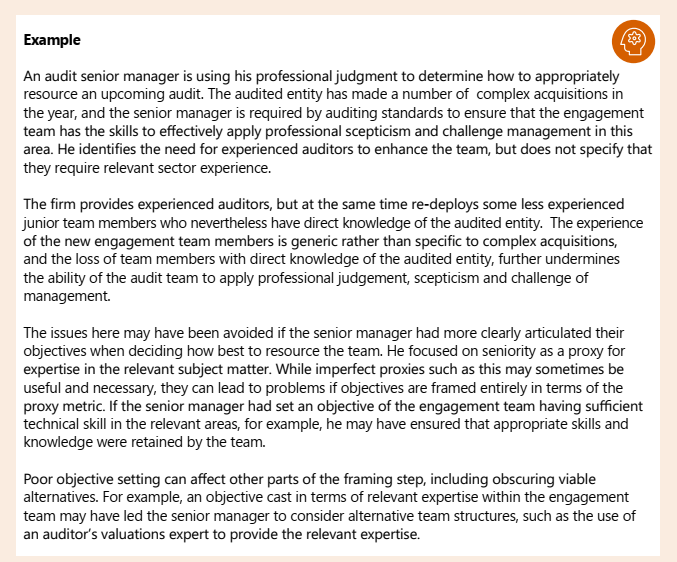

Framing the Issue: Defining the problem, articulating objectives, and identifying all viable alternatives to avoid narrow thinking.

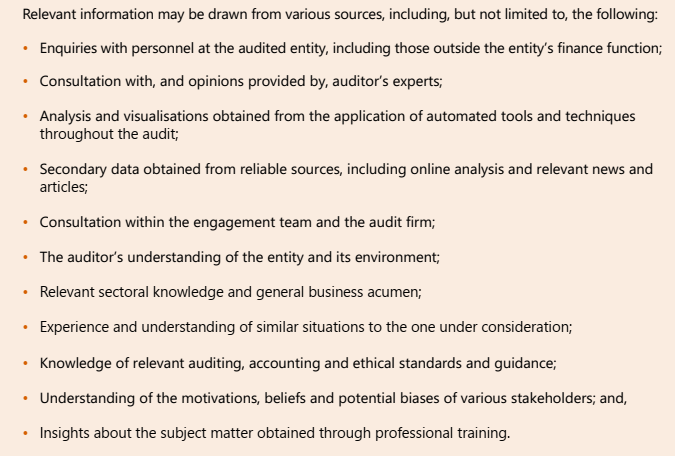

Marshalling Information: Seeking out diverse data sources, including “external signals” outside the entity’s finance function.

Analysis and Evaluation: Evaluating the relevance and reliability of the gathered information in the context of the judgement.

Stand Back and Conclude: Pausing to view the preliminary conclusion in the round to ensure it hasn’t been unduly affected by bias or time pressure.

Document, Communicate, and Reflect: Recording the rationale for the decision, explaining it to stakeholders, and reflecting on the process to improve future judgements.

3) Consultation

Quality is significantly enhanced by discussion. Engaging with technical panels, experts, or engagement quality reviewers helps mitigate individual biases and fosters a culture of healthy debate within the firm.

4) Environmental Factors

Auditors do not work in a vacuum. The framework acknowledges that firm culture, time constraints, and the integrity of management at the audited entity all significantly impact how challenging it is to exercise quality judgement.

Illustrative Examples in Practice

To show how these principles apply in the real world, the FRC provides three fictional scenarios.

Example 1: The “Window Dressing” Disclosure

Scenario: A manufacturing company significantly increases its cash balance just before year-end by delaying supplier payments and offering customer discounts, resulting in a deceptively low “net debt” figure in the notes.

The Judgement: The auditor must decide if the disclosure is materially misstated because it obscures the entity’s true financial position throughout the year.

The Application: The auditor demonstrates scepticism by questioning management’s “commercial reasons” and researches industry peers to see how they disclose average net debt. This highlights the need to “frame” the issue around user needs and fair presentation rather than just technical accuracy.

Example 2: The “Close-Call” Going Concern

Scenario: A group recovers from the pandemic but faces debt refinancing risks. Management claims there is no material uncertainty, pointing to informal bank support and shareholder letters of intent.

The Judgement: The engagement partner must determine if a “material uncertainty” exists regarding going concern.

The Application: Despite intense pressure from management to sign off quickly, the partner consults with her firm’s ethics and technical teams. This illustrates how environmental factors (time pressure) can threaten quality and the importance of using safeguards like consultation to mitigate threats to objectivity.

Example 3: The Hostile Audit Committee

Scenario: Following a delay in an audit caused by late and incomplete management papers on goodwill impairment, a hostile Audit Committee threatens to put the audit out to tender.

The Judgement: The audit firm must decide whether to continue the relationship for the next year.

The Application: An internal panel assesses the integrity of the client’s governance and the appropriateness of the team’s challenge. This example warns against “motivated reasoning”—the firm must ensure that financial priorities (profitability of the audit) do not lead to an inappropriate decision to continue if the client lacks integrity or ethical values.