FRS 102 is a financial reporting standard that was introduced in the United Kingdom in 2013. It replaces previous UK GAAP and is designed to bring UK accounting standards in line with International Financial Reporting Standards (IFRS). FRS 102 is divided into four parts:

The Framework for the Preparation and Presentation of Financial Statements

This part of FRS 102 sets out the overall principles that guide the preparation and presentation of financial statements. It includes guidance on the conceptual framework underlying financial reporting, the concepts of capital maintenance and accrual accounting, and the principles of going concern, prudence, and consistency.

The Presentation of Financial Statements

This part of FRS 102 covers the specific requirements for the presentation of financial statements. It includes guidance on the format and content of the balance sheet, income statement, and statement of changes in equity, as well as the notes to the financial statements.

The Recognition and Measurement of Assets and Liabilities

This part of FRS 102 sets out the principles for the recognition and measurement of assets and liabilities. It includes guidance on the recognition of various types of assets and liabilities, such as property, plant, and equipment, intangible assets, financial assets, and provisions. It also provides guidance on the measurement of assets and liabilities, including the use of historical cost, fair value, and present value.

The Disclosure of Accounting Policies and Other Notes

This part of FRS 102 covers the requirements for the disclosure of accounting policies and other notes to the financial statements. It includes guidance on the types of accounting policies that must be disclosed, the format and content of the accounting policies note, and the presentation of other notes to the financial statements.

Overall, FRS 102 provides a comprehensive set of principles and requirements for the preparation and presentation of financial statements in the United Kingdom. It is designed to improve the transparency and comparability of financial reporting, and to bring UK accounting standards in line with international best practices.

Generally its quite hard to predict whether or not there will be a recession with a high degree of accuracy. For example, whilst its possible some people may have predicted the recessions after credit crisis and Covid-19, they would have been a shock to the vast majority of small and medium sized businesses. However, in 2022 there are clear signs that a recession is on the way and the Bank of England almost appears to be relying on this to bring inflation under control.

Economic outlook

The ONS has reported that Gross Domestic Product (GDP) grew by just 0.1% in February 2022, following 0.8% growth in January 2022. GDP then fell by 0.1% in March 2022 and 0.3% in April 2022.

Worryingly services, production and construction were all negative in April 2022, the first time since January 2021 during the height of the pandemic.

We won’t find out about the GDP May and June 2022 for quite some time, but early indications are that consumer confidence are at a record low.

This is unsurprising given the impact of soaring inflation of 9.1% in May 2022, the highest in 40 years, resulting in real incomes falling for most households and the cost of living crisis.

With interest rates also rising and likely to increase further, many consumers and also businesses can be expected to batten down the hatches by reducing discretionary spending and cutting back in general.

In previous recessions we have seen that deals fell through because companies didn’t want to take on risk, they wanted to save cash and to basically weather the storm. Although the Covid-19 pandemic and multiple lockdowns killed off numerous businesses, some of those which survived are in a perilous state with high levels of debt and may not survive another recession.

Preparing for a possible recession

Although most of our clients are generally in a good position, its always good to review finances. The points below are not very complex, but mainly guard against complacency.

Review cashflow/forecasts

Review your costs such as staff, rent, overheads etc and gross profit margins and work backwards to calculate how much income is needed in the next 1 year to stay afloat:

established businesses will also need to make a profit to pay dividends etc

startups will need to review runway and cash burn

Stress test these calculations, what happens if you lose some customers, or some deals in the pipeline fall through, or there are unexpected costs or investors fall through?

Is there a cash shortfall? If so, how can the gap be filled?

Financing

Many established businesses run up large aged debtors balances as they don’t want to aggressively chase their customers, and they know that they will usually pay in the end. However, in times of economic uncertainty its best not to hold off too long and regularly chase customers for payment. What happens if your customer’s customer doesn’t pay them? Credit control can be done in a polite manner, without threatening court etc.

Maximise your funding and check your access to loans, overdrafts and credit cards etc. It can be a good idea to have facilities on tap, in case you need them. With interest rates at a low level, the cost of financing a loan to sit in your bank during the next 1-2 years could give you peace of mind if you have a low cash balance.

Sales and marketing

Established businesses can sometimes run on autopilot, but customer behaviour has been shown to change during times of recession or economic uncertainty. Clients or customers may focus on low cost but conversely high quality/reliability/luxury etc can sometimes become more important for other customers. How can you use this to your advantage? Are there any niches or customer segments you can target?

Look after your core customers, keep them happy and help their businesses and they’ll stick around/survive as customers.

It may not be possible to enter a completely new market, but businesses may be able to use their skills and capacity in different ways. For example, during lockdown high quality fresh food suppliers to restaurants and hotels lost their customers, but a whole new consumer market opened up for home deliveries.

Costs

Review your staff contracts and consider how the redundancy process could work, in the worst case scenario. If you have under performing staff, put communications with them in writing about their performance and take legal advice. Its best to prepared just in case.

After the pandemic, many businesses are already quite lean but there could be some projects or spending which could be delayed.

Marketing spend is a tricky one, it can often take spending money to make money! Its easy to leave Adwords/Social media spending running in the background, but now is definitely a good time to review the effectiveness of marketing campaigns and check how they are performing.

We cannot include car repair, fuel and running costs in a limited company’s accounts unless they are for a company car.

Directors can claim for 45p per mile for the first 10,000 business miles per year and 25p thereafter.

We would normally make an adjustment for this via the director’s loan account and then the director can be re-imbursed or withdraw funds from the company when it suits them.

Why can’t we include fuel and motor expenses for personal cars?

If a car is owned personally by a director, then they are personally responsible for paying the general running costs for the car, such as:

petrol or diesel fuel

car insurance

MOT and servicing

general repairs

A director may think that if they are using their car for business use, for example for travelling to meetings with clients and temporarily working at a client site (ie less than 2 years), then they should be able to claim a proportion of the running costs in their company’s accounts.

However, unlike use of home, we cannot apportion a percentage of the director’s personal car running costs for business use.

Calculating mileage allowance

The Government has set specific rates of mileage allowances and these are supposed to cover the cost of fuel and also the general running costs.

For example, if a director drives 15,000 business miles per year, the mileage allowance would be:

10,000*45p + 5,000*25p = £5,750

Estimating mileage allowance

It is best to keep a detailed log of business journeys, for example, using a mileage calculator app or a spreadsheet.

However, it is also possible to estimate the business mileage.

1) Use something like Google Maps to calculate the distance to each client and then estimate the number of journeys. For example: Distance*2 (for return journey) * number of journeys per week * 52 (or eg 48 after holidays etc) = estimated number of business miles

2) If the above is very tricky, some clients also use a general round number percentage based on their perception of how much they use the car for business, for example 80% business use.

It is also important to remember that HMRC could potentially disallow the tax deduction if they do not agree with the basis or estimate.

Value Added Tax is an indirect tax aimed at consumers.

If a business meets certain criteria then it has to charge VAT on its sales of goods and services.

In a supply chain there are usually a series of businesses selling to each other until the final product or service reaches the consumer.

Generally, businesses can reclaim the VAT they incur on their costs of sales and overhead at each step of the supply chain and so ultimately the consumer is the one who ends up bearing the cost of VAT.

VAT is a regressive tax and typically makes up a larger proportion of budget for a low income household compared to a high income household.

VAT rules

The key legislation is the Value Added Tax Act 1994 (“VAT’94”). There are also Statutory Instruments and in certain cases the detailed rules are set out in HMRC notices and leaflets.

HMRC’s notices are very helpful to explain the rules and are aimed at businesses, whilst their internal manuals also go into significant detail. There is also a lot of case law where HMRC or taxpayers have taken each other to court over how the rules are interpreted.

Whereas many other taxes and accounting rules are principles based, VAT is almost rules based due to the large number of specific rules set out in legislation and case law to cover specific circumstances and scenarios.

Output VAT

Businesses have to charge VAT on their goods and services if they meet the criteria below. The most common rate of VAT is 20%, so if their net price excluding VAT is £100, they would need to charge a gross price of £120 including VAT.

Key criteria for charging VAT

Under s.4 VAT’94, VAT shall be charged on any supply of goods or services made in the United Kingdom where:

it is a taxable supply,

made by a taxable person,

in the course or furtherance of any business carried on by him.

If these criteria are not met, a supply is outside the scope of VAT, and VAT registration is not possible.

1) Taxable supply A taxable supply is a supply of goods or services made in the United Kingdom other than an exempt supply (s.4(2) VAT’94). Consideration must be charged for services rendered, even if its only £1. Free services are excluded from VAT.

There is a list of exempt supplies in Schedule 9 of VAT’94.

In addition to exempt supplies, certain sales made outside of the UK may also be outside the scope of VAT.

2) Taxable person A business would be a taxable person if it is able to register for VAT, either voluntarily or compulsorily.

Its compulsory for a business to register for VAT if their annual sales exceed £85,000.

3) In the course or furtherance of any business HMRC have set out a number of key questions based on case law, such as:

Does the activity have a certain measure of substance in terms of the quarterly or annual value of taxable supplies made?

Is the activity conducted in a regular manner and on sound and recognised business principles?

Is the activity predominately concerned with the making of taxable supplies for a consideration?

Input VAT

To achieve the economic target of indirectly taxing consumers, businesses can reclaim the VAT that they pay to their suppliers, if they meet certain criteria. So if the gross purchase cost is £120, including VAT, then they can reclaim £20 VAT, so their net cost is £100.

Input VAT is the total VAT suffered on purchases, but these could be incurred in relation to taxable supplies, exempt supplies or non-business activities.

Under S.26(1),(2) VAT’94 a business can reclaim input VAT attributable to taxable supplies in the course or furtherance of their business (i.e. the same supplies on which output VAT is charged as defined in S.4 VAT’94 mentioned above). This is known as “input tax”.

Input VAT cannot be reclaimed on expenditure relating to: • activities outside of VAT or non-business activities • blocked items such as cars and entertaining • exempt activities unless they are below a set level (de minimis of £625 on average per month and half of total input tax in period)

VAT Registration & administration

If a business makes taxable supplies and they are provided in the course of business, then they can register for VAT.

A business would then account for VAT by adding 20% (usually) output tax to their sales invoices and submitting a return to HMRC on a periodic basis (normally quarterly). On the return, they would then reclaim input tax, which is the VAT on purchases related to the provision of taxable supplies.

If output tax exceeds input tax, then a business would need to pay this excess to HMRC.

If input tax is higher, HMRC would pay the difference to the business.

On the VAT registration form an effective date is chosen (can be in the past) and VAT needs to be accounted for after this date. However, input VAT can also be reclaimed for expenses related to taxable supplies in the 6 months prior to registration.

Summary of the new IFPR rules in relation to own funds and liquid assets

IFPR relates to the Investment Firms Prudential Regime.

From 1 January 2022, FCA authorised investment firms which are not MiFID exempt will need to comply with the new rules1 for MIFIDPRU investment firms. So this will affect most current EUR50k, EUR125k and EUR750k firms as well as Exempt CAD firms.

Firms will need to monitor their level of own funds and ensure that these are higher than their own funds requirements.

For small firms this is similar to the old capital adequacy rules and ICAAP, but the minimum levels are higher and there are some other differences as well. Exempt CAD firms won’t be able to rely on professional insurance and so their capital requirement will be much higher.

At least 1/3 of the fixed overhead requirement also has to be held as liquid assets such as cash and trade debtors (with 50% haircut).

If a firm’s level of own funds drops below 110% of the requirement then this will trigger an early warning with the FCA. If the firm’s own funds or liquid assets fall below a certain level then the firm would need to wind down.

Own funds

Own funds mainly relate to the Equity section of a firm’s balance sheet. Most of our clients will typically have common equity tier 1 capital but we don’t expect many to have significant levels of Additional Tier 1 (eg certain types of preference shares) or Tier 2 capital (eg subordinated debt due after 5 years.

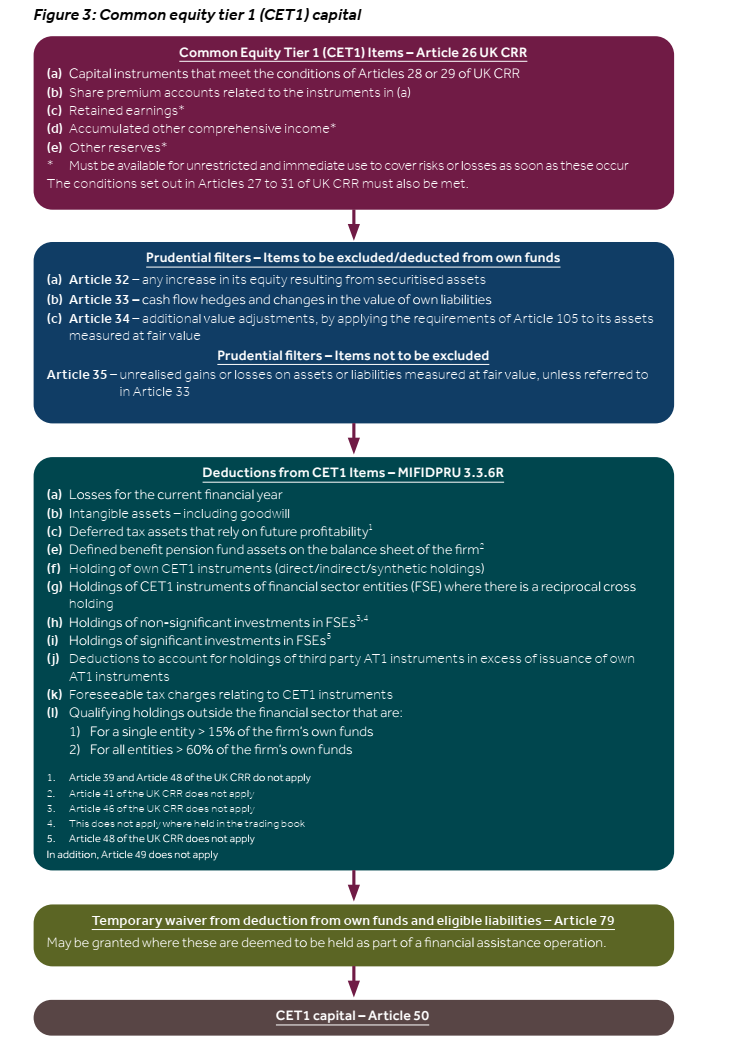

Common equity tier 1 capital

This is share capital, share premium, retained earnings and other reserves less deductions for losses of the current financial year and certain assets such as intangible assets, deferred tax, pension assets, investments in financial firms and a number of others etc (see FCA handbook MIFIDPRU 3.3.6 for the full list). The FCA’s CP20/24 also has Figure 3:

It may also be possible to include interim profits and new capital instruments (eg ordinary shares) with permission from the FCA. See FCA handbook MIFIDPRU 3.3.2 and 3.3.3 and for the forms. The FCA handbook mentions they expect to receive a notification at least 20 business days before the issuance.

The independent auditors would also need to verify the profit and write a letter to confirm the profit figure.

Own funds requirement

Firms will have to maintain own funds that at least equal to their own funds requirement. For small investment firms which meet the SNI criteria2 this is the higher of:

permanent minimum capital (“PMR”)

fixed overheads requirement (“FOR”)

Permanent minimum capital (“PMR”)

For most small firms their PMR will be £75,000 if they do not hold client money/securities and are not placing orders on a firm commitment basis. (ie similar to EUR50k firms under old rules)

If firms hold client money and also cannot operate matched principal trading or dealing on their own account their PMR will be £150,000.

For other firms their PMR will be £750,000.

See MIFIDPRU 4.4.1 for full details. There are also transitional arrangements so that the PMR does not need to be held straight away on 1 January 2022. See the FCA Handbook MIFIDPRU TP 2 and also CP20/24 Chapter 6.

Fixed overheads requirement (“FOR”)

The FOR is the minimum level a firm would need to absorb losses if it has to wind down or exit the market. Firms will need to consider this in detail in their Internal Capital Adequacy and Risk Assessment (ICARA) process.

The FOR is calculated as 1/4 of its relevant expenditure in the previous year as per its most recent audited accounts.

This will exclude fully discretionary expenditure such as as:

staff bonuses and variable remuneration

non recurring expenses from non-ordinary activities

amortisation where intangibles are already deducted from own funds

See MIFIDPRU 4.5.3 for full details.

Basic liquid assets requirement

Firms need to hold in core liquid assets at least 1/3 of their fixed overhead requirement plus 1.6% of the total amount of any guarantees provided to clients.

Core liquid assets are mainly cash and SNIs can also use short term trade receivables due within 30 days, subject to a 50% haircut (ie like a bad debt provision). The assets also need to be denominated in pound sterling, so this would exclude cash or trade receivables in USD or EUR for example.

Cash needs to be short term deposits in held at a UK authorised credit institution. Certain money market funds can also be used.

See MIFIDPRU 6.2.1 onwards.

Overall financial adequacy rule

Firms would need to assess various business risks in detail as part of the ICARA process. This is a very complex and wide area, and only covered briefly here.

A firm needs to hold sufficient own funds and liquid assets for the firm to remain financially viable throughout the economic cycle and to allow it to be wound down in an orderly manner, if needed.

The amount of own funds needed is the:

amount of own funds needed to fund ongoing business and cope with periods of stress; and

the amount of own funds needed to allow it to wind down in an orderly manner

The own funds threshold requirement is the amount of own funds needed to enable a firm to comply with the overal financial adequacy rule.

FCA Handbook MIFIDPRU 7.6.4 also has this picture:

The amount of liquid funds needed is the basic liquid assets requirement plus the higher of:

an amount of liquid assets needed to fund ongoing business and cope with periods of stress

additional amount of liquid assets needed to allow it to wind down in an orderly manner

It can also include non-core liquid assets in the calculation, see MIFIDPRU 7.7.8.

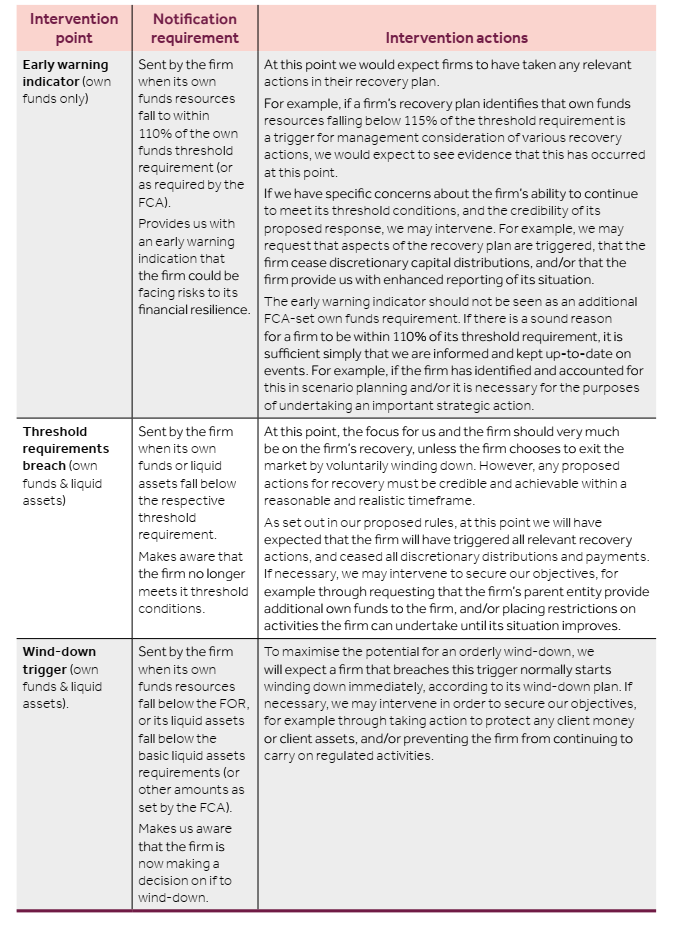

Notfying the FCA & Triggers

Firms must notify the FCA if the liquid assets or own funds fall below certain limits. A wind down would also be triggered if they fall too low.

CP21/7 has the following table which summarises the rules:

The FCA Handbook often refers to “UK CRR”. CRR stands for Capital Requirements Regulations and was originally EU legislation. After Brexit the UK has its own version.

UK CRR is the UK version of Regulation of the European Parliament and the Council on prudential requirements for credit institutions and investment firms (Regulation (EU) No 575/2013) and amending Regulation (EU) No 648/2012, which is part of UK law by virtue of the EUWA, read together with any CRR rules as defined in section 144A of the Act.

As a starting point, the EU CRR Articles define the types of capital and then the adjustments required can generally be found in the FCA Handbook.

If you give money to charity then you can obtain tax relief if you are a higher rate taxpayer and the donation was made to a registered charity in the EU (plus Norway, Iceland and Liechtenstein).

You can also obtain relief for donations made to Community Amateur Sports Clubs (CASCs) that were registered with HMRC when you made the donation.

Paperwork

You’ll need to make a gift aid declaration to the charity, whether its in writing/electronic/verbal and you should also receive and keep a receipt for the donation.

Tax relief

Your basic rate limit will be increased by the donation, grossed up by the basic rate 20%, and this means that you will save tax.

For example, if you give £1,000 to charity and are a 40% taxpayer, your basic rate will be increased by £1,000 x 100/80 = £1,250. The tax saving is then £1,250 x (40%-20%) = £250

Carry back to previous tax return

You can claim gift aid early by including it in your previous tax return upto 31 January.

For example, you make a donation in October 2021, and you can claim it in the 2010/21 tax return (instead of waiting until the following year for 2021/22 tax return).

Shares/property

There are sometimes reliefs available, but you should check the rules

Fees related to a trade are often allowable but it depends on the nature of the fees. Generally, fees related to the purchase or sale of property/assets and to do with raising equity finance are disallowed for tax purposes.

“Capital” expenditure: not deductible

Legal and professional fees are “capital” if they relate to an asset’s:

acquisition

improvement

elimination

And the asset is of an enduring nature and will yield benefits to the business for a number of years in the future.

For example, property, computer/office equipment, fixtures and fittings, licences (eg FCA) and other assets are all capital items. So legal and professional fees incurred in relation to these are also of a capital nature.

Fees related to leasing a property/asset, raising shares and share options are also capital.

Therefore, these kinds of fees would all be disallowed for tax purposes.

Although fees for intangible assets are disallowed initially, there may be an amortisation expense that is allowable, for example when licences or IPR are written off over their useful lives.

“Revenue” expenditure: are deductible

If fees don’t relate to capital then they can normally be deducted if they relate to the trade.

So fees for a non-business purpose wouldn’t be allowed.

Examples of allowable legal/professional fees include:

It may sometimes be important to check if the invoice finance is recourse or non-recourse. Examples of lenders are Market Invoice, Bibby, Lloyds etc.

But for smaller businesses, the typical accounting treatment will involve:

sales invoice is raised: debit trade debtor and credit sales as normal

invoice finance received: debit cash and credit liability for invoice lender

customer pays the invoice: debt cash/liability for invoice lender and credit trade debtor

Step 3 depends on whether the customers pay the business or to the invoice lender directly (for example into a trust account)

Care should be taken to ensure that the full detail of the above transactions are recorded, and not just a shortcut. For example, unwitting clients/bookkeepers may post the cash received from the invoice lender against the trade debtor. But this would mean that the liability is omitted.

During the monthly/annual accounts preparation the interest and fees on the invoice finance should also be calculated and reconciled to a statement from the invoice lender, along with the period end liability.

If your company makes a loss from its trading operations then it can claim relief against corporation tax.

Current year

If you make a trading loss, you can offset the loss against profits/gains from other trades or sources in your company in the current year.

Carry back against previous year

If you can’t use up all your losses in the current year, you can also carry them back against the total profits of the previous year. If you already paid tax for the previous year, then you could get a cash refund from HMRC.

To do this, you’d need to enter the loss to be carried back in your current year’s tax return, tick a repayment is due and then either amend the previous year’s tax return or make a claim under s.37 of CTA. If not amending the previous year, you can try to make the claim by making a note in the trading losses section of the tax computation and if this doesn’t work you’d need to write to HMRC.

There is a time limit of making the claim within 2 years of the end of the accounting period when the loss was made. Eg a loss in YE 31/12/2021 needs to be claimed by 31/12/2022.

If you can’t use the losses in the current/previous year, you can also carry them forward to be offset against future profits relating to the same trade.

For example, if you make a loss in a consulting trade, this can’t be offset against a new trade in future relating to e-commerce.

Key legislation: CTA 2010 s.35 onwards

Property income losses

If you have a loss from renting out a property (eg house/flat or shop/office) then it can be offset against trading profit or other income (from the same property business) in the current year or in future years.loss

But it cannot be carried back.

Capital losses

If you make a capital loss, for example from selling shares or property at a loss, then these can only be offset against capital gains arising in the current year or in the future.

They cannot be carried back and they cannot be used against trading profits or other income.

bad debts that definitely cannot be recovered (eg debtor has already closed down)

specific bad debts that are doubtful/unlikely to be received

debts released by the creditor as part of a statutory insolvency arrangement

Bad debts won’t receive tax deductions if they’re general provisions against overall trade debtors. For example, total trade debtors are £10,000 and a general bad provision is created for £1,000.

Specific bad debt provisions

Before the accounts are finalised the trade debtors are normally reviewed for recoverability. If there a debt which is unlikely to be paid then a specific bad debt provision is usually created. For example, Company X Ltd’s debt of £595 is written off.

This reduces trade debtors in the balance sheet and involves a bad debt expense in the P&L.

This bad debt expense will be included in the tax return as an allowable deduction.

Timing

The ability of the debtor to pay has to be evaluated as at the year end. So if the debtor only ran into financial difficulties after the year end, then the bad debt expense wouldn’t be allowed as a tax deduction.

Slow payer

HMRC do not consider that a debtor being a slow payer is grounds for a debt being doubtful.

Waiver

If a debt is written off for reasons other than the debtor facing financial difficulties then HMRC could challenge any tax deduction, for example, if the debtor is related to the business (family connections or parent/subsidiary).

Evidence required

The business should retain evidence supporting a specific bad debt provision such as:

correspondence with the debtor

legal letters

credit reports

board minutes reviewing aged debtors

If HMRC challenge a bad debt, they would seek to establish the following details about individual bad debts:

how the extent of its doubtfulness was evaluated, and

when this was done, and

by whom, and

what specific information was used in arriving at that valuation.

Key legislation

S35, S259 Income Tax (Trading and Other Income) Act 2005, S55, S303, S479 Corporation Tax Act 2009