Summary of the new IFPR rules in relation to own funds and liquid assets

IFPR relates to the Investment Firms Prudential Regime.

From 1 January 2022, FCA authorised investment firms which are not MiFID exempt will need to comply with the new rules1 for MIFIDPRU investment firms. So this will affect most current EUR50k, EUR125k and EUR750k firms as well as Exempt CAD firms.

Firms will need to monitor their level of own funds and ensure that these are higher than their own funds requirements.

For small firms this is similar to the old capital adequacy rules and ICAAP, but the minimum levels are higher and there are some other differences as well. Exempt CAD firms won’t be able to rely on professional insurance and so their capital requirement will be much higher.

At least 1/3 of the fixed overhead requirement also has to be held as liquid assets such as cash and trade debtors (with 50% haircut).

If a firm’s level of own funds drops below 110% of the requirement then this will trigger an early warning with the FCA. If the firm’s own funds or liquid assets fall below a certain level then the firm would need to wind down.

Own funds

Own funds mainly relate to the Equity section of a firm’s balance sheet. Most of our clients will typically have common equity tier 1 capital but we don’t expect many to have significant levels of Additional Tier 1 (eg certain types of preference shares) or Tier 2 capital (eg subordinated debt due after 5 years.

Common equity tier 1 capital

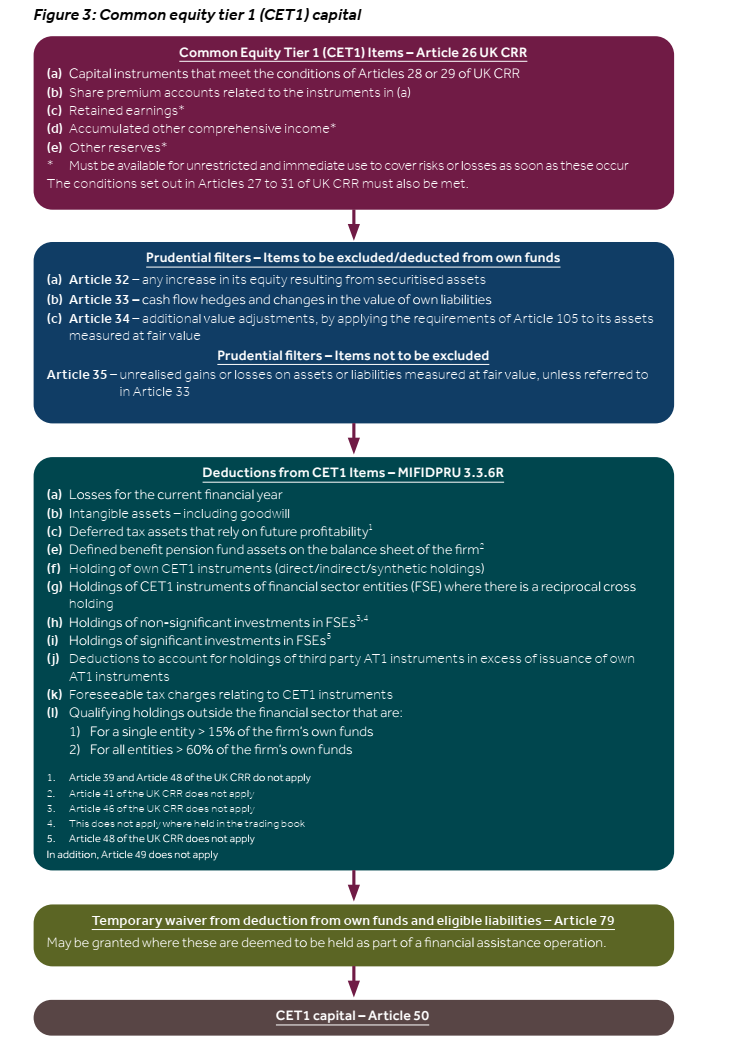

This is share capital, share premium, retained earnings and other reserves less deductions for losses of the current financial year and certain assets such as intangible assets, deferred tax, pension assets, investments in financial firms and a number of others etc (see FCA handbook MIFIDPRU 3.3.6 for the full list). The FCA’s CP20/24 also has Figure 3:

It may also be possible to include interim profits and new capital instruments (eg ordinary shares) with permission from the FCA. See FCA handbook MIFIDPRU 3.3.2 and 3.3.3 and for the forms. The FCA handbook mentions they expect to receive a notification at least 20 business days before the issuance.

The independent auditors would also need to verify the profit and write a letter to confirm the profit figure.

Own funds requirement

Firms will have to maintain own funds that at least equal to their own funds requirement. For small investment firms which meet the SNI criteria2 this is the higher of:

- permanent minimum capital (“PMR”)

- fixed overheads requirement (“FOR”)

Permanent minimum capital (“PMR”)

For most small firms their PMR will be £75,000 if they do not hold client money/securities and are not placing orders on a firm commitment basis. (ie similar to EUR50k firms under old rules)

If firms hold client money and also cannot operate matched principal trading or dealing on their own account their PMR will be £150,000.

For other firms their PMR will be £750,000.

See MIFIDPRU 4.4.1 for full details. There are also transitional arrangements so that the PMR does not need to be held straight away on 1 January 2022. See the FCA Handbook MIFIDPRU TP 2 and also CP20/24 Chapter 6.

Fixed overheads requirement (“FOR”)

The FOR is the minimum level a firm would need to absorb losses if it has to wind down or exit the market. Firms will need to consider this in detail in their Internal Capital Adequacy and Risk Assessment (ICARA) process.

The FOR is calculated as 1/4 of its relevant expenditure in the previous year as per its most recent audited accounts.

This will exclude fully discretionary expenditure such as as:

- staff bonuses and variable remuneration

- non recurring expenses from non-ordinary activities

- amortisation where intangibles are already deducted from own funds

See MIFIDPRU 4.5.3 for full details.

Basic liquid assets requirement

Firms need to hold in core liquid assets at least 1/3 of their fixed overhead requirement plus 1.6% of the total amount of any guarantees provided to clients.

Core liquid assets are mainly cash and SNIs can also use short term trade receivables due within 30 days, subject to a 50% haircut (ie like a bad debt provision). The assets also need to be denominated in pound sterling, so this would exclude cash or trade receivables in USD or EUR for example.

Cash needs to be short term deposits in held at a UK authorised credit institution. Certain money market funds can also be used.

See MIFIDPRU 6.2.1 onwards.

Overall financial adequacy rule

Firms would need to assess various business risks in detail as part of the ICARA process. This is a very complex and wide area, and only covered briefly here.

A firm needs to hold sufficient own funds and liquid assets for the firm to remain financially viable throughout the economic cycle and to allow it to be wound down in an orderly manner, if needed.

The amount of own funds needed is the:

- amount of own funds needed to fund ongoing business and cope with periods of stress; and

- the amount of own funds needed to allow it to wind down in an orderly manner

The own funds threshold requirement is the amount of own funds needed to enable a firm to comply with the overal financial adequacy rule.

FCA Handbook MIFIDPRU 7.6.4 also has this picture:

The amount of liquid funds needed is the basic liquid assets requirement plus the higher of:

- an amount of liquid assets needed to fund ongoing business and cope with periods of stress

- additional amount of liquid assets needed to allow it to wind down in an orderly manner

It can also include non-core liquid assets in the calculation, see MIFIDPRU 7.7.8.

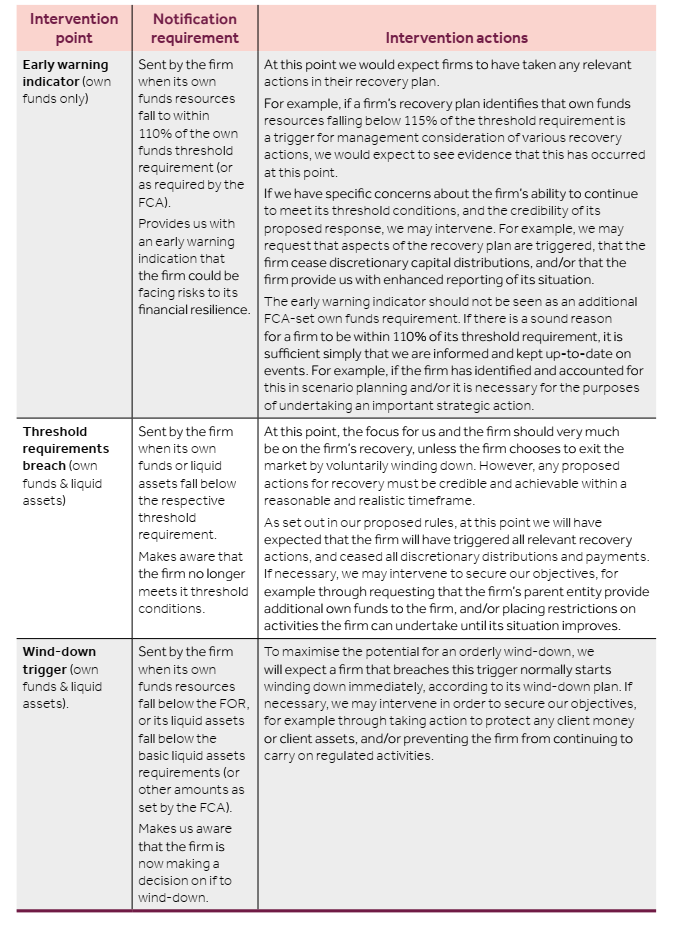

Notfying the FCA & Triggers

Firms must notify the FCA if the liquid assets or own funds fall below certain limits. A wind down would also be triggered if they fall too low.

CP21/7 has the following table which summarises the rules:

1Where can we find the rules?

The easiest place to start is the FCA Handbook MIFIDPRU Prudential Sourcebook for MiFID Investment Firms.

There are also further explanations in the FCA’s consultation and policy papers on IFPR CP20/24, CP21/7 and PS21/17.

The FCA Handbook often refers to “UK CRR”. CRR stands for Capital Requirements Regulations and was originally EU legislation. After Brexit the UK has its own version.

UK CRR is the UK version of Regulation of the European Parliament and the Council on prudential requirements for credit institutions and investment firms (Regulation (EU) No 575/2013) and amending Regulation (EU) No 648/2012, which is part of UK law by virtue of the EUWA, read together with any CRR rules as defined in section 144A of the Act.

As a starting point, the EU CRR Articles define the types of capital and then the adjustments required can generally be found in the FCA Handbook.

The actual UK legal instruments are also noted on the FCA’s website about IFPR.

2SNI firms

There are a number of conditions, but the main ones are:

- average assets under management less than £1.2 billion

- client orders handled are less than £100m per day for cash trades and £1 billion per day for derivatives

- does not have permission to deal on its own account

- balance sheet total (including off balance sheet items) less than £100m

- annual revenue is less than £30m