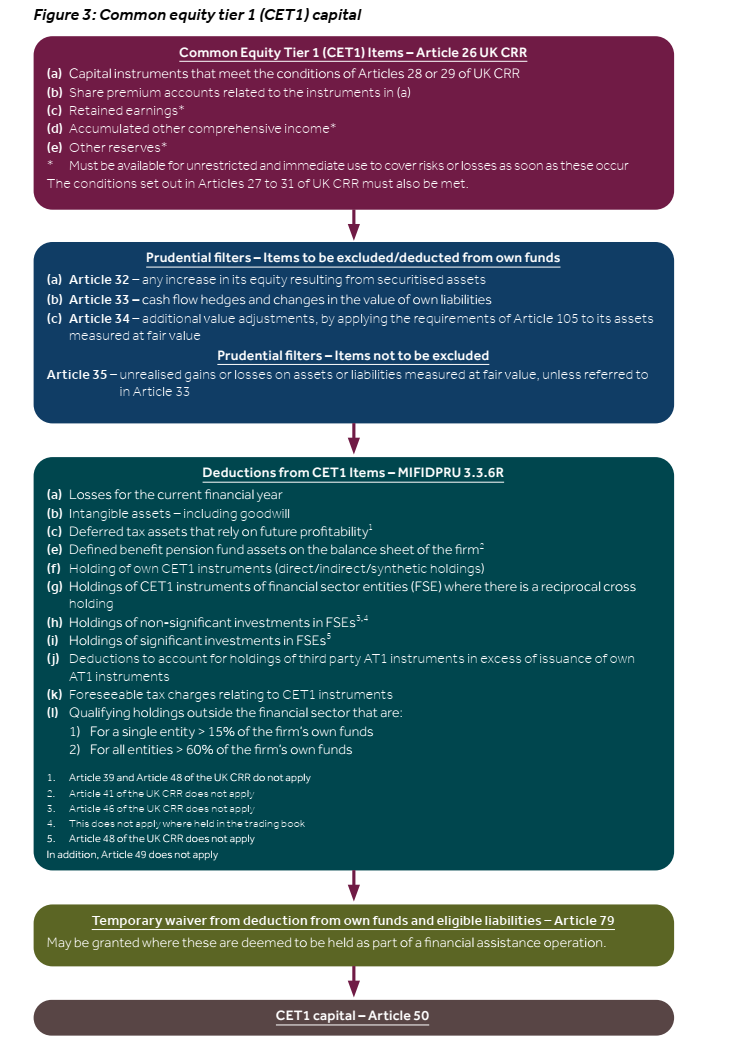

Requirements

For investment firms regulated under the FCA’s Prudential sourcebook for MiFID Investment Firms (MIFIDPRU), managing liquidity is a critical and constant obligation. The regime mandates that firms hold a sufficient buffer of high-quality liquid assets to ensure they can withstand a period of financial stress. While holding cash is the most straightforward way to meet these requirements, it can be inefficient, offering little to no return on significant capital balances.

A strategic alternative is the use of Short Term Money Market Funds (MMFs). When selected carefully, certain MMFs can offer a yield on regulatory capital while fully satisfying the stringent liquidity rules. This article provides a technical overview of how MIFIDPRU firms can use MMFs to meet their Basic Liquid Assets Requirement.

The Basic Liquid Assets Requirement under MIFIDPRU 6

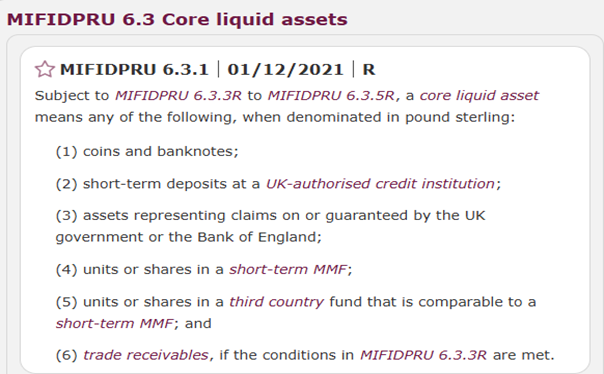

The core of the liquidity framework is found in MIFIDPRU 6. It requires a MIFIDPRU investment firm to hold, at all times, an amount of “core liquid assets” that is at least equal to one-third of its Fixed Overheads Requirement (FOR). For firms providing certain guarantees to clients, an additional 1.6% of the total value of those guarantees must also be held in liquid assets. This is known as the Basic Liquid Assets Requirement.

The definition of “core liquid assets” is highly prescriptive. According to rule MIFIDPRU 6.3.1, these assets are strictly limited to:

While all categories are important, the use of MMFs warrants particular attention due to the potential for enhanced yield combined with regulatory compliance.

What Constitutes a “Short-Term Regulated Money Market Fund”?

The most critical aspect for firms to understand is that “short-term regulated money market fund” is a specific regulatory designation, not a general marketing term. For a fund to be eligible as a core liquid asset, it must be formally authorized as a “Short-Term Money Market Fund” under the UK Money Market Funds Regulation (UK MMF Regulation).

This regulation imposes stringent requirements on the fund’s structure and portfolio, designed to ensure high levels of liquidity and low risk. Key criteria include:

- Portfolio Composition: The fund must invest in a portfolio of high-quality, short-term assets such as government securities, certificates of deposit, commercial paper, and repurchase agreements (repos).

- Maturity Limits: The fund must adhere to strict maturity limits for its portfolio, including a Weighted Average Maturity (WAM) of no more than 60 days and a Weighted Average Life (WAL) of no more than 120 days.

- Credit Quality: The fund is restricted to investing in instruments of high credit quality, subject to a formal internal credit assessment process.

- Diversification: The regulation mandates strict diversification rules to mitigate concentration risk to any single issuer or counterparty.

Funds that do not meet these criteria, even if they are marketed as “cash-like” or “money market” funds, will not qualify as core liquid assets.

Practical Application: Distinguishing Eligible from Ineligible Funds

The distinction between qualifying and non-qualifying funds is best illustrated with practical examples.

- Potentially Eligible Fund: A fund structured as a UCITS ETF that explicitly states its objective is to provide returns in line with money market rates by investing directly in a portfolio of high-quality, short-term debt instruments, deposits, and repos. Such a fund is designed to operate within the constraints of the UK MMF Regulation and is a strong candidate for eligibility.

- Ineligible Fund: A synthetic ETF that aims to replicate an overnight interest rate using financial derivatives, such as swaps. This type of fund does not hold a portfolio of underlying cash or debt instruments. Due to its synthetic nature and the inherent counterparty risk associated with swaps, it cannot meet the strict portfolio composition and credit quality criteria required for authorization as a Short-Term MMF under the UK MMF Regulation. Therefore, it would be ineligible as a core liquid asset.

Due Diligence: The Non-Negotiable Step

Before a firm includes any MMF in its liquidity calculation, it must perform thorough due diligence. This involves obtaining and scrutinizing the fund’s official documentation, specifically the Key Investor Information Document (KIID) and the full prospectus.

These documents must contain an explicit statement confirming that the fund is authorized as a “Short-Term Money Market Fund” under the UK MMF Regulation. Without this confirmation, the investment cannot be treated as a core liquid asset.

Regulatory Treatment: Haircuts and Reporting

The regulatory treatment for qualifying MMFs is highly favorable. Under MIFIDPRU 7, units in a qualifying short-term regulated money market fund are subject to a 0% haircut. This means they can be valued at 100% of their current market value for the purpose of the Basic Liquid Assets Requirement calculation, effectively treating them as equivalent to a cash deposit.

Conversely, if an asset does not meet the strict definition of a core liquid asset, it is not a matter of applying a higher haircut. The asset is simply ineligible and cannot be included in the calculation at all. Attempting to include a non-qualifying fund, such as a synthetic ETF, would result in a breach of the firm’s liquidity requirements.

Conclusion

For MIFIDPRU investment firms, utilizing Short-Term Money Market Funds can be a prudent and effective strategy for managing regulatory liquidity. It allows firms to move beyond the zero-return environment of cash holdings and earn a yield on their mandatory liquid asset buffer.

However, this strategy is contingent on rigorous due diligence. Firms must look beyond marketing descriptions and verify the precise regulatory status of any fund under the UK MMF Regulation. By ensuring that investments strictly qualify, firms can confidently optimize their liquidity management, enhance capital efficiency, and remain fully compliant with their prudential obligations.

Please contact us for a free, no obligation consultation to discuss your requirements: 0207 100 3610