We act as auditors to small cap plcs listed on AQSE, AIM and Euronext and also as reporting accountants on IPOs. In this post we explore the Aquis Stock Exchange (“AQSE”) in more detail.

What is AQSE?

AQSE is a fast growing stock exchange which targets growth companies which are small to medium in size. Its a Registered Investment Exchange in the UK and is regulated by the FCA. Companies listed on AQSE are eligible investments for the full range of unlisted company tax reliefs, including EIS, capital gains, stamp duty and inheritance tax.

Market overview

As at February 2023 there were 105 companies listed on AQSE with an average market cap of £16m.

1 or 2 new companies tend to list every month and they typically raise £1m-£3m upon listing. There were 22 new issues in 2022, raising a total of £31m.

Existing companies often need to raise further money, for example to help with expansion, finance acquisitions or to fund working capital and there were £32m further issues in 2022. In Feb’23 Invinity Energy Systems Plc raised £21.5m in a very successful share issue.

Trading activity

The chart below shows that there are typically 2,000 to 3,000 trades per month with a total value ranging from £10m to £20m. However, we note that AQSE is generally seen as less liquid than larger stock markets.

Why list on AQSE?

Simply put, its far cheaper and faster to list on AQSE compared to AIM or LSE.

After the FCA’s rule changes its also become much more difficult for companies to raise money on LSE as there is a minimum market cap of £30m.

Whereas companies listing on AQSE only need a minimum market cap of £700,000.

We also note that AQSE is gradually growing whereas AIM is in danger of declining. AIM used to have 3,600 companies listed at one time, but its less than 900 currently.

Is it worth listing?

Historically our tech startup clients have raised money from VCs and angels, ranging from £100k upto £70m. AQSE probably wouldn’t be the first option for a tech startup, but it may be worth exploring, especially if a company is starting to generate revenue but might not be able to achieve the typical hockey stick growth that VCs expect.

Established companies from other sectors have tended to rely on bank loans, bonds or convertible loans, but they have generally needed significant assets or personal guarantees in order to raise finance. So if a company doesn’t have significant assets then AQSE would definitely be worth exploring.

But if loan finance is available, the loan interest costs and related covenants are likely to be cheaper and less complex than listing on AQSE.

The downsides of listing

The listing process requires a lot of time and effort from management and all the advisory fees and listing expenses typically start from around £80k-£100k. Most of the listing costs would be deducted from the IPO but some of the initial costs would need to be prepaid before the IPO can get fully underway. Although founders may be able to seek pre-IPO fundraising from investors to help with the initial listing costs.

Once listed, a company has to comply with strict AQSE rules and has to make regular announcements about its activities and certain events. There are also very tight deadlines for publishing interims and annual accounts.

Summary of the new IFPR rules in relation to own funds and liquid assets

IFPR relates to the Investment Firms Prudential Regime.

From 1 January 2022, FCA authorised investment firms which are not MiFID exempt will need to comply with the new rules1 for MIFIDPRU investment firms. So this will affect most current EUR50k, EUR125k and EUR750k firms as well as Exempt CAD firms.

Firms will need to monitor their level of own funds and ensure that these are higher than their own funds requirements.

For small firms this is similar to the old capital adequacy rules and ICAAP, but the minimum levels are higher and there are some other differences as well. Exempt CAD firms won’t be able to rely on professional insurance and so their capital requirement will be much higher.

At least 1/3 of the fixed overhead requirement also has to be held as liquid assets such as cash and trade debtors (with 50% haircut).

If a firm’s level of own funds drops below 110% of the requirement then this will trigger an early warning with the FCA. If the firm’s own funds or liquid assets fall below a certain level then the firm would need to wind down.

Own funds

Own funds mainly relate to the Equity section of a firm’s balance sheet. Most of our clients will typically have common equity tier 1 capital but we don’t expect many to have significant levels of Additional Tier 1 (eg certain types of preference shares) or Tier 2 capital (eg subordinated debt due after 5 years.

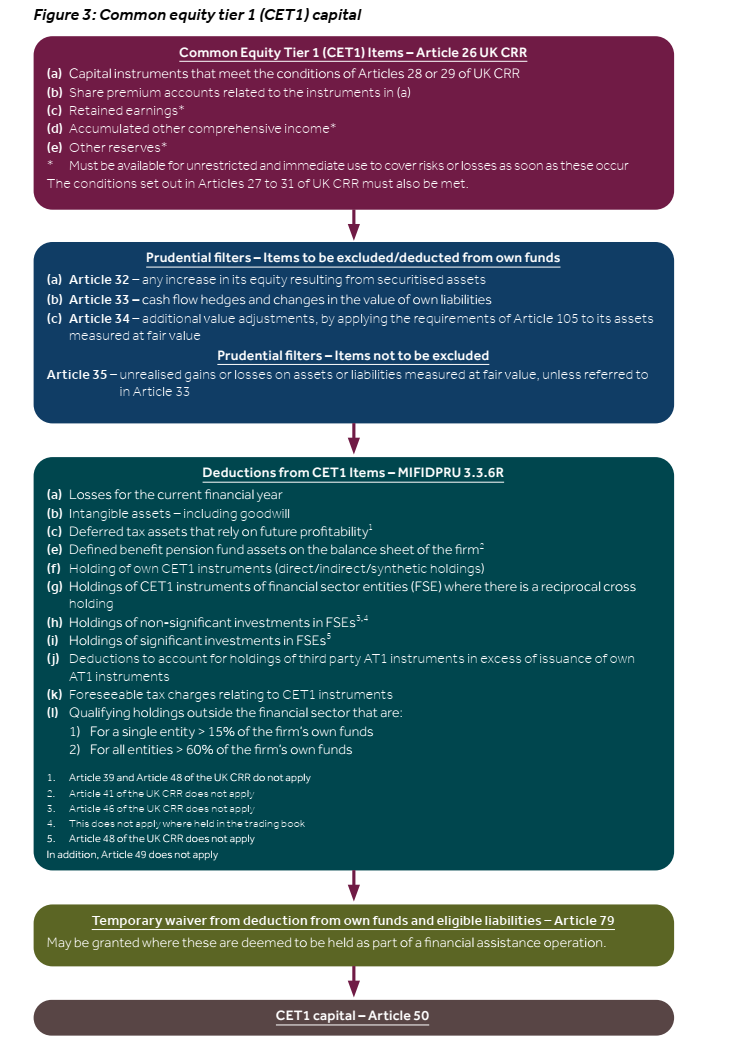

Common equity tier 1 capital

This is share capital, share premium, retained earnings and other reserves less deductions for losses of the current financial year and certain assets such as intangible assets, deferred tax, pension assets, investments in financial firms and a number of others etc (see FCA handbook MIFIDPRU 3.3.6 for the full list). The FCA’s CP20/24 also has Figure 3:

It may also be possible to include interim profits and new capital instruments (eg ordinary shares) with permission from the FCA. See FCA handbook MIFIDPRU 3.3.2 and 3.3.3 and for the forms. The FCA handbook mentions they expect to receive a notification at least 20 business days before the issuance.

The independent auditors would also need to verify the profit and write a letter to confirm the profit figure.

Own funds requirement

Firms will have to maintain own funds that at least equal to their own funds requirement. For small investment firms which meet the SNI criteria2 this is the higher of:

permanent minimum capital (“PMR”)

fixed overheads requirement (“FOR”)

Permanent minimum capital (“PMR”)

For most small firms their PMR will be £75,000 if they do not hold client money/securities and are not placing orders on a firm commitment basis. (ie similar to EUR50k firms under old rules)

If firms hold client money and also cannot operate matched principal trading or dealing on their own account their PMR will be £150,000.

For other firms their PMR will be £750,000.

See MIFIDPRU 4.4.1 for full details. There are also transitional arrangements so that the PMR does not need to be held straight away on 1 January 2022. See the FCA Handbook MIFIDPRU TP 2 and also CP20/24 Chapter 6.

Fixed overheads requirement (“FOR”)

The FOR is the minimum level a firm would need to absorb losses if it has to wind down or exit the market. Firms will need to consider this in detail in their Internal Capital Adequacy and Risk Assessment (ICARA) process.

The FOR is calculated as 1/4 of its relevant expenditure in the previous year as per its most recent audited accounts.

This will exclude fully discretionary expenditure such as as:

staff bonuses and variable remuneration

non recurring expenses from non-ordinary activities

amortisation where intangibles are already deducted from own funds

See MIFIDPRU 4.5.3 for full details.

Basic liquid assets requirement

Firms need to hold in core liquid assets at least 1/3 of their fixed overhead requirement plus 1.6% of the total amount of any guarantees provided to clients.

Core liquid assets are mainly cash and SNIs can also use short term trade receivables due within 30 days, subject to a 50% haircut (ie like a bad debt provision). The assets also need to be denominated in pound sterling, so this would exclude cash or trade receivables in USD or EUR for example.

Cash needs to be short term deposits in held at a UK authorised credit institution. Certain money market funds can also be used.

See MIFIDPRU 6.2.1 onwards.

Overall financial adequacy rule

Firms would need to assess various business risks in detail as part of the ICARA process. This is a very complex and wide area, and only covered briefly here.

A firm needs to hold sufficient own funds and liquid assets for the firm to remain financially viable throughout the economic cycle and to allow it to be wound down in an orderly manner, if needed.

The amount of own funds needed is the:

amount of own funds needed to fund ongoing business and cope with periods of stress; and

the amount of own funds needed to allow it to wind down in an orderly manner

The own funds threshold requirement is the amount of own funds needed to enable a firm to comply with the overal financial adequacy rule.

FCA Handbook MIFIDPRU 7.6.4 also has this picture:

The amount of liquid funds needed is the basic liquid assets requirement plus the higher of:

an amount of liquid assets needed to fund ongoing business and cope with periods of stress

additional amount of liquid assets needed to allow it to wind down in an orderly manner

It can also include non-core liquid assets in the calculation, see MIFIDPRU 7.7.8.

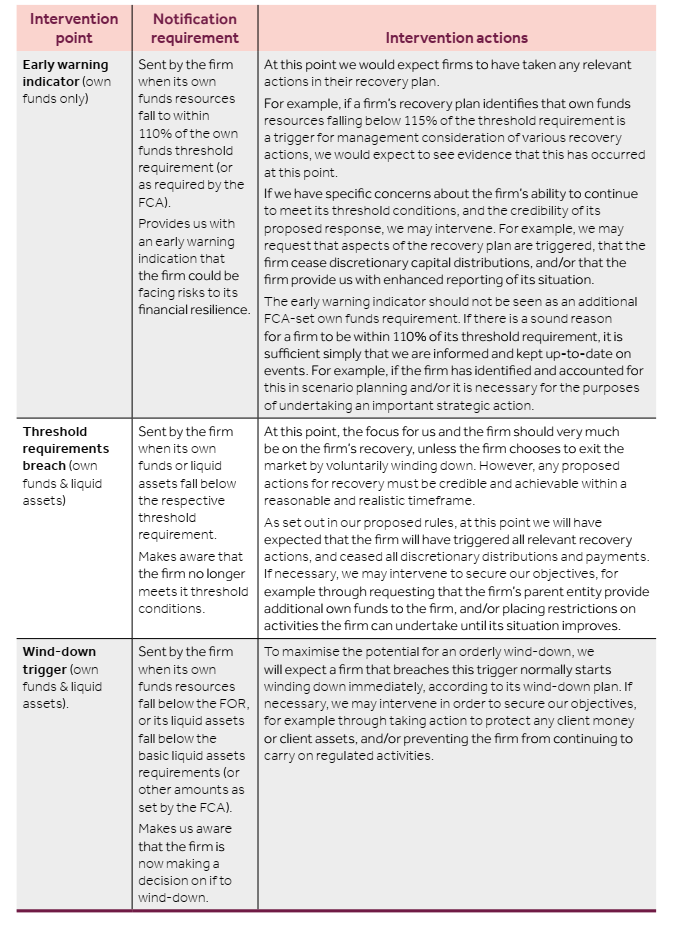

Notfying the FCA & Triggers

Firms must notify the FCA if the liquid assets or own funds fall below certain limits. A wind down would also be triggered if they fall too low.

CP21/7 has the following table which summarises the rules:

The FCA Handbook often refers to “UK CRR”. CRR stands for Capital Requirements Regulations and was originally EU legislation. After Brexit the UK has its own version.

UK CRR is the UK version of Regulation of the European Parliament and the Council on prudential requirements for credit institutions and investment firms (Regulation (EU) No 575/2013) and amending Regulation (EU) No 648/2012, which is part of UK law by virtue of the EUWA, read together with any CRR rules as defined in section 144A of the Act.

As a starting point, the EU CRR Articles define the types of capital and then the adjustments required can generally be found in the FCA Handbook.

Setting up a new startup or business can be stressful with what looks like a mountain of paperwork and red tape to deal with.

We’re here to help you with the tax and accounting side of things and have advised startups as diverse as a new hotel chain to a payments platform to fashion stores and e-commerce. We can support you with the fund raising process from seed rounds all the way through to an IPO.

[maxbutton id=”1″ url=”https://www.mah.uk.com/prices/” text=”Get an Instant Quote” ]

Generally speaking, if you make money from a business then you have to pay tax on your profit.

Profit is defined for tax purposes as your sales and business income minus eligible business expenses. Most expenses incurred in running a business will save tax, but some are disallowed such as entertaining customers/suppliers with restaurants, events or gifts.

Business structure

Limited company

The vast majority of our clients are limited companies because this structure can save a lot of tax and offer a lot of flexibility.

If you want to scale and grow quickly via investment then you’ll need a limited company to issue shares to investors. You can also use a holding company to own subsidiaries if you may need to sell in future or will have different sites/sectors.

Limited companies also provide protection against personal assets (eg house/car) if the business goes bust and can’t pay its suppliers/lenders.

you can decide how much money to take out the business and when

delay/defer tax using a directors loan

appoint family members as shareholders/directors to save tax

EIS/SEIS tax breaks

R&D tax credits

Limited companies are required to file annual accounts and corporation tax returns, as well as file an annual confirmation statement. There is also more documentation involved to deal with shares and directors will need to file a self assessment to declare their dividends.

Sole trader

Sole trader registration is best for very small businesses as it involves less admin and cost.

If you expect your profit to exceed the annual personal allowance (2019: approx £12k per year) then you’ll need to be registered with HMRC as a sole trader.

Once your turnover exceeds £40-50k per year then it will usually be worth converting to a limited company.

If you expect to make a loss in the first few years then sole trader status can be quite beneficial as you offset the losses against previous years employment income to get tax refunds.

The main filing requirement is to prepare a self assessment tax return with details of income and expenses.

VAT

If your sales will exceed a certain threshold (£85k per year in 2019) then you have to be registered for VAT. This means you have to hand over 20% of your sales to HMRC, but you can also reclaim input VAT on expenses.

Most of our B2C clients will therefore add 20% to their planned sales prices so that they don’t suddenly start making a loss once VAT registration kicks in or lose consumers from having to increase prices. For B2B clients its not really an issue as business customers can generally just reclaim the VAT.

Many of our startup clients have voluntarily registered for VAT so that they can get regular refunds from HMRC for VAT paid on their expenses such as rent, software and consultancy etc.

VAT returns and payments usually have to be made quarterly.

Payroll

If you hire staff then you have to setup a PAYE scheme and issue payslips to employees. You’ll also need to calculate their income tax and national insurance and pay this to HMRC every month.

A pension scheme will also need to be setup and staff enrolled, although they can choose to opt out if they prefer.

Most of our limited company clients will setup a PAYE, even if there are no staff, as directors can pay themselves a salary to save tax.

Record keeping

As you can see above, various documents have to be filed with HMRC for accounts, self assessement and VAT etc on a regular basis.

In order to prepare these documents we need to have the full records of the business including:

bank payments and receipts

sales

expenses

loans

share issues/options

Most clients will enter the transactions into cloud software like Xero, or use our excel template. Some clients are too busy or hate bookkeeping and so we do it for them.

Managing performance

If the bookkeeping is done regularly then we can check how the business is performing. We can also prepare cashflow forecasts and predict how the business will do in the next year.

This is important because the vast majority of startups fail in the first 3 years, but as we help clients to manage their performance, our clients tend to survive and thrive.

For example, we noticed one of our clients had a lot of slow paying customers with low value invoices and helped them to setup direct debit collections to automate the process. On another client we helped them to analyse their margins and to increase prices.

Next steps

[maxbutton id=”1″ url=”https://www.mah.uk.com/prices/” text=”Get an Instant Quote” ]

Please contact us for a free, no obligation consultation to discuss your requirements. Our offices are at Liverpool Street or we’re happy to have a phone/email discussion.

Although the MiFID II regulation has been published since 2014 (delayed implementation date – 3rd January 2018), it is surprising that H M Revenue & Customs has not yet provided any firm guidance on the VAT treatment of research work.

Recent press states that HMRC is now meeting with industry groups and is set to publish guidance on the VAT treatment of research work carried out from 3 January 2018 onward under MiFID II.

Commission sharing agreements (CSA)

Currently, any research work paid via a CSA is potentially an exempt supply for VAT purposes as it is normally bundled with a payment for execution services. Execution commissions are exempt supplies for VAT and if research is part and parcel of the execution services, then the bundled research services are also exempt from VAT. MiFID II seeks to separate research from commissions as part of a larger aim to reduce the research data being fed to fund managers.

Fund managers

Firms that manage funds are generally not eligible to register for VAT as they mainly deal in financial products, which are exempt from VAT.

MiFID II requires that the payment for research work is done separately and independently from the payment of commissions for execution services. Research Payment Accounts (RPA) are now going to be used by many fund managers.

VAT position after MiFID II?

If research is to be identified as a separate supply from that of execution services, HMRC rules could deem the supply of research services as VATable services at the standard rate of 20%.

The disadvantage here would be felt by research providers as:

Fund managers will not be willing to increase their budgets for research given that they are unable to reclaim any VAT suffered on research costs,

Research providers would be pricing themselves out of market (against providers outside Europe) should they try and increase their prices by 20% in order to accommodate the possible new VAT burden, and

as a result, UK based research providers will be forced to absorb the 20% VAT burden and accept lower fees than what they are receiving now.

We are keenly following this issue for our clients. If you require any assistance with your company’s VAT or tax position in respect of work in the Financial Services industry, please contact us.

This post only applies to off payroll “contractors” (including locums or consultants etc) who are working in the public sector, such as for the NHS, a government agency, university or local authority and use a limited company to raise invoices.

Contractors working in the private sector will not currently be affected by these rules, although there could potentially be a risk of similar legislation in the future for the private sector.

Old IR35 rules

The old IR35 rules are explained in detail here, but basically if a contractor can demonstrate that they are not a “shadow employee” because they have rights of control over how/when they work, rights of substitution and no mutual obligations then they can raise an invoice via a limited company and avoid payroll taxes.

Under the old rules it was up to the contractor to decide if they were inside or outside of IR35, and so they could use their judgement or obtain professional advice about this. If HMRC disagreed with the contractor and believed that they were inside IR35, then the liability for unpaid salary taxes was on the contractor.

New IR35 rules from 6 April 2017

If the new rules are found to apply, then contractors will have to pay employment taxes similar to those paid via payroll/PAYE, even if they are using a limited company.

Under the new rules, it is up to the public sector body to decide if the contractor is inside or outside of IR35.

If the public sector body is later found to have made an incorrect decision then they will be held liable for the unpaid salary tax/NIC. Therefore, it will be less risky for public bodies to apply a blanket rule of paying all contractors as employees and deducting tax/NIC, rather than verifying whether each and every single contractor is outside IR35 and paying the full invoice amount.

Our understanding is that the NHS and locum agencies will be generally by paying all doctors and nurses via PAYE under the new rules. IT and other consultants may also be caught by the NHS or other public bodies.

Impact of new IR35 rules for public sector contractors

The fee payer (eg NHS or agency) will calculate income tax and employee NIC and deduct these from the fee payable to the contractor. The contractor’s limited company will get a tax deduction for the income tax and NIC, but will then have to pay a further 20% corporation tax on the profit.

However, if all the public sector net income is withdrawn as salaries then there will not be any profit left and this is exempt from income tax/NIC as it has already been deducted at source.

The 5% allowance normally available to contractors inside IR35 is also removed for public sector contracts.

Overall, we CANNOT see any significant benefitsfrom using a limited company if a contractor will be caught by the new rules. The normal tax planning using dividends or multiple shareholders will be affected by the extra corporation tax that is payable on top of income tax/NIC unless all net income is withdrawn as salaries.

In this case, the contractor would be better off being employed directly via the agency/NHS without the limited company. The limited company can also be closed down.

We use our expertise to help clients maximise their assets where legally possible in accordance with UK GAAP or IFRS. This is especially useful for companies who need to meet gross asset or capital requirements such as FCA firms or raising bank loans or complying with bank or investor covenants. However, the methods below are not always possible and there will also be tax consequences.

The methods below are of a permanent or long term nature and do not involve window dressing or other short term methods, so the accounts should still be true and fair and have a clean audit report if all the relevant criteria are met.

1) Recognise intangible assets

If your company has spent time or money developing intellectual property then the chances are that it can be capitalised on the balance sheet if certain criteria are met.

For example, one of our clients spent £200k developing an online payments platform as well as other mobile apps. We reviewed the contracts and looked at how the systems worked and after discussions with management were able to confirm that an intangible asset had been created. One of the main factors in particular was that the platform was already generating significant revenue, however, even if a company is loss making or a startup it may still be able to capitalise intangibles depending on their profit forecasts.

Staff time can also be capitalised. For example on an FCA client, we looked at how much time a director and his staff spent on building and developing a complex quantitative model to monitor financial trading signals as opposed to maintaining it and fixing bugs. We were then able to advise on the percentage of staff costs that could potentially be capitalised.

Intangible assets such as those above can also qualify for tax relief on amortisation.

We also found that a mining client had spent significant amounts on legal fees and we were able to capitalise these as exploration and evaluation assets.

2) Turn tax losses into a deferred tax asset

If its probable that the company will generate sufficient profits in the future to utilise tax losses then the future tax benefit can be recognised as an asset.

This one is often tricky to convince auditors (such as ourselves!) but at the end of the day, if cashflow forecasts are good enough to satisfy going concern, then they could potentially support a deferred tax asset especially if a company is beginning to turn a corner and is close to generating profits.

3) Make sure all income has been accrued

If you bill clients at the end of a job then you could potentially have work in progress at the end of the year which has a value. This will often have to be brought into your revenue stream anyway to ensure that income is recognised in the period in which it is generated.

Some companies may have intercompany fees, licences or royalties charged to foreign subsidiaries or connected companies. For example, one of our clients has a UK system and we helped them to setup a licencing fee to a foreign company under an intercompany agreement. This will increase turnover and assets as long as the debt is recoverable. For a profit making group this won’t be a problem, however, if there is no chance that the subsidiary or connected company can pay the fees in future, then the debt will need to be written off or impaired.

4) Convert debt to equity (or subordinate it)

If directors have used their own funds to finance a company then this will be a liability on the balance sheet. One simple way to boost the balance sheet and to reduce creditors is by issuing shares to the director in exchange for writing off the debt. This would also avoid a tax bill which could occur if the debt was written off to the profit and loss. If the shares are issued at market value then this will also avoid income tax for the director.

FCA firms can also subordinate the debt for at least 5 years to include it in their capital calculations and we can advise on how to do this using a subordinated loan agreement.

One of our clients tried to do this using preference shares, however, care needs to be taken because if they are redeemable preference shares then the debt component still needs to be presented as a liability on the balance sheet.

5) Revalue property

If your company owns its own premises or has investment properties then these can usually be revalued upwards based on management’s estimates. A more formal independent valuation may also be required in certain circumstances.

6) Issue shares!

We left this one till last as it sounds a bit obvious but many of our clients have raised funding from investors, for example £100k-£200k from angel/seed investors, £0.5m from VCs and £m’s from AIM. If you’re unsure of the process, we can help you to prepare a pitch deck and financial projectors and help you to approach potential investors.

We can give you tailored advice to boost your balance sheet

As you can see we use our specialist expertise in a joined up way to think about accounting and tax requirements. The above examples can sometimes get quite tricky so its definitely worthwhile seeking professional advice. You can contact us here for further information.

As readers are no doubt aware the UK voted to leave the EU in June 2016. We were shocked that Brexit actually happened and were worried about the impact on our clients.

The long lasting effects are unknown and much will depend on the negotiation of trade agreements with the EU. Some commentators have suggested that the UK could be in recession for many months whilst others have suggested that this will all blow over and the UK will rapidly recover.

We have attempted to evaluate the worst case scenarios and impact on our small business clients.

We all need to be aware of the potential threats to the UK economy and our clients/customers and take appropriate steps in order to survive and to thrive.

Summary

The Bank Of England is likely to cut interest rates and provide liquidity facilities to banks in order to prevent another credit crisis and to calm the markets. Financial markets could be due to political or financial/economic reasons and its too early to predict what could happen in the future.

However, there is a potential risk of recession due to the fall in exchange rates, inflationary pressure and uncertainties affecting business and consumer confidence. Foreign investment may also fall.

The full impact of Brexit is not yet known and one of the key factors will be the negotiations of a new trade agreement with the EU. If the Norway/Swiss models are followed and UK businesses can access the Single Market for imports/exports and financial passporting then the impact of Brexit may be limited.

However, we have considered the worst case scenarios for our core sectors:

Financial services: In the short term, FCA firms should re-check financial forecasts, risk assessments and capital adequacy requirements. In the medium/long term they will need to consider whether they will need to migrate to the EU or setup a subsidiary to ensure passporting.

Tech startups: In the short term, cash burn and forecasts should be re-assessed as it could potentially become more difficult to raise finance if investors are nervous about the UK economy. In the long term, restrictions on movement of labour could reduce the talent pool and some of the infrastructure and benefits of operating in the UK.

Fintech: Could suffer the same problems as tech startups but could also be affected by lack of passporting or reduced demand from the financial services sector if they are suffering from Brexit.

Import / Export: Amazon sellers could suffer from double layers of taxation and tariffs if they’ll now have to export goods to both the UK and EU separately, depending on how trade agreements are negotiated. Foreign goods could also become more expensive to UK customers, reducing to demand.

Contractors: Economic uncertainty could increase demand for temporary contracts if businesses are adverse to hiring new permanent staff. However, financial services could potentially suffer from job losses and temporary staff could also be affected. EU citizens need to check if they can stay in the UK and may be able to apply for permanent residence.

AIM/ISDX plcs: Equity markets have suffered and existing plcs may find it difficult to raise new capital. If the credit crisis of 2007-08 can be used as a guide then it may be difficult for new firms to list or to reverse in the near future, as many deals collapsed after the credit crisis.

There are different factors involved in setting up company structure and it depends on the type of business, circumstances of the shareholders and their aims for the business.

Shareholders:

if you may sell the company and re-invest the profits a holding company may be useful

otherwise, the co-founders can be the shareholders

for contractors and family owned businesses, husband/wife can be shareholders to maximise dividends

ambitious startups looking to grow should setup a share cap table

leave an option pool for key staff

eg 2 co-founders setup a company owning 45% each and leave 10% option pool

Multiple trades:

Clients often have more than 1 business. The simple and efficient solution is to have 1 company and run the different businesses as divisions of this company.

For tax purposes, the different trades need to have separate profit and loss calculations. This is because losses from a trade can be set against the profits from another trade in the same year. But if losses are carried forward against future profits they can only be used against profits from the same trade.

If you’ll be expecting to sell a business/trade, it can be hived out into a separate company before sale. If its held for at least 1 year before sale, then there is no tax due to Substantial Shareholding Exemption.

Sometimes its better to start off with a group structure, so 1 holding company and 3 subsidiaries for the different businesses/trades, although this can also be achieved later on.

Dividends:

Profits after tax can be given to shareholders, and this is normally the most tax efficient way to extract profits.

Dividends have to be paid according to shareholding. So if a husband and wife hold 50% each, they have to receive equal dividends. Sometimes, it may make sense for 1 spouse to hold 100% shares and shares can be transferred between spouses without tax at any time (with the right paperwork) to maximise differences in tax rates and allowances.

If you’ll be receiving investment, the investors will also be able to receive dividends. So if you have a separate side business operating out of the same company, it will normally be better to hive this out before receiving investment.

Need help?

If you need more help on setting up company structure then please contact us for a free consultation.

For example, we note that online gambling was initially illegal in many jurisdictions around the world, but one by one, governments have been licensing operators and subjecting them to heavy taxes.

However, even if Bitcoin audits do not become mandatory, it could become best practice for Bitcoin businesses to undergo an audit of their financial statements. Many Bitcoin exchanges have already had independent tests to prove their level of Bitcoin reserves so the next step could be to have their financial statements audited.

A Bitcoin audit could be also be required in the UK if a company exceeds the small company limits or is deemed to be an ineligible company.

What does an audit of financial services generally involve?

In the UK, a company has to produce a set of annual accounts in accordance with generally accepted accounting principles (eg UK GAAP or IFRS) and Companies Act 2006. However, if a financial director produces a set of accounts, how would a user or reader of the accounts know whether or not they can trust its contents?

An auditor will independently verify whether the accounts are true and fair and in compliance with the applicable laws and regulations. The auditor will need to be suitably qualified, be named on the Audit Register and will need to perform the audit in accordance with International Standards on Auditing.

An auditor will obtain a full understanding of the business and the industry in order to perform a risk analysis and to plan the audit. They’ll need to consider what the key balances and transactions are and which ones are most susceptible or fraud or error.

Once the audit has been planned they’ll work through the accounts to verify and corroborate the assets, liabilities income and expenses that have been included in the accounts and also to test for any significant transactions or balances which have been omitted.

Key risks for a Bitcoin audit

A Bitcoin business would have assets, liabilities and transactions denominated in Bitcoin. Key risks would include whether Bitcoin assets (eg reserves in cold storage) and liabilities (eg customer deposits) exist, are correctly valued and whether they are complete.

It may be possible to obtain sufficient, appropriate evidence about existence and completeness for exchanges by using an approach similar to that used by Stefan Thomas and his tools such as Easy Audit. Other Bitcoin businesses may need different techniques. Depending on the type of Bitcoin business and the complexity of its transactions, an auditor may require a cryptographer or IT specialist to perform such procedures in order to comply with ISA 620.

Bitcoins are likely to be treated as a cash equivalent/ foreign currency or as an investment, depending on how the business uses them and its intentions. In order to ensure they’re correctly valued, they would need to be translated into the base currency used in the financial statements (eg £ in the UK) and an adjustment may be required depending on the accounting policy.

A Bitcoin business is likely to be involved in online transactions and the transfer of funds, so internal controls and anti-money laundering procedures are also likely to be key areas for a Bitcoin audit.

We can help

Our team have audited both financial services businesses and e-commerce businesses and can use this experience to help us audit a Bitcoin business efficiently and effectively.

For example, a large online gaming businesses had millions of customer accounts and we had to verify the total liabilities owed to customers, as well as testing a sample of individual deposit/withdrawal transactions and interactions with payment gateways.

The financial services businesses we audit have complex accounting/tax rules such as mark to market/fair value and also strict rules for anti-money laundering and dealing with client money.

Please contact us for assistance and we’ll be happy to offer a free consultation where possible.

As Xero accountants we specialise in tech startups but also have experience of many other types of businesses from creative agencies to contractors to restaurants.

What is Xero?

Xero makes it very easy for businesses to do their bookkeeping, for example by automatically feeding in transactions from your bank and using plugins to connect with your business.

Tax

We can review what you’ve done in the cloud as your Xero accountants and provide expert tax and VAT advice to make sure that:

1) everything is in compliance with tax legislation

2) tax savings are made wherever possible

Business advice

Xero also has lots of great charts and reports and we’ll run through your business with you to analyse your performance and discuss how you can grow or face challenges.

Save 15%

Did you know that Xero offers a discount on all cloud accounting packages signed up by Xero accountants? We pass on those savings to our clients whilst many other firms keep the discount to boost their own profits.

Our fees start from £50/mth + VAT for dealing with accounts and corporation tax (excluding the Xero fee) for simple startups.

Contact us

Please contact us for a free, no obligation consultation to discuss your requirements and to setup or switch your Xero account. Our base at Liverpool Street is just a short walk away from Silicon Roundabout.